Fisher's z-distribution

Fisher's z-distribution is the statistical distribution of half the logarithm of an F-distribution variate:

|

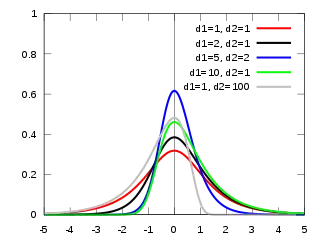

Probability density function  | |||

| Parameters | deg. of freedom | ||

|---|---|---|---|

| Support | |||

| Mode | |||

Ronald Fisher

It was first described by Ronald Fisher in a paper delivered at the International Mathematical Congress of 1924 in Toronto.[1] Nowadays one usually uses the F-distribution instead.

The probability density function and cumulative distribution function can be found by using the F-distribution at the value of . However, the mean and variance do not follow the same transformation.

The probability density function is[2][3]

where B is the beta function.

When the degrees of freedom becomes large () the distribution approaches normality with mean[2]

and variance

Related distribution

- If then (F-distribution)

- If then

References

- Fisher, R. A. (1924). "On a Distribution Yielding the Error Functions of Several Well Known Statistics" (PDF). Proceedings of the International Congress of Mathematics, Toronto. 2: 805–813. Archived from the original (PDF) on April 12, 2011.

- Leo A. Aroian (December 1941). "A study of R. A. Fisher's z distribution and the related F distribution". The Annals of Mathematical Statistics. 12 (4): 429–448. doi:10.1214/aoms/1177731681. JSTOR 2235955.

- Charles Ernest Weatherburn (1961). A first course in mathematical statistics.

External links

This article is issued from Wikipedia. The text is licensed under Creative Commons - Attribution - Sharealike. Additional terms may apply for the media files.