Dynamic currency conversion

Dynamic currency conversion (DCC) or cardholder preferred currency (CPC) is a process whereby the amount of a Visa or MasterCard transaction is converted by a merchant or ATM to the currency of the payment card's country of issue at the point of sale.

DCC allows the merchant, merchant's bank or ATM operator to charge a markup on the exchange rate used, sometimes by as much as 18%.[1] Where the DCC markup is less than the card issuer's currency conversion fee, DCC can benefit card holders by allowing them to see the amount that their card will be charged expressed in the currency of the card's country of issue. However, in most cases, DCC markups are higher than the card issuer's currency conversion fee (which can be zero), thereby negating this benefit.

DCC services are generally provided by third party operators in association with the merchant, and not by a card issuer. Card issuers do not provide cardholders with a DCC option at the point of sale, but these two card networks permit DCC operators to offer currency conversion in accordance with their card processing rules.[2][3]

Without DCC, the currency conversion is carried out by the card issuer when the transaction is charged to the card holder's statement, usually a day or two later, but for an increasing number of cards in real time. Even though the card issuer will publish the exchange rate used for conversion on the statement, most do not disclose the exchange rate used to convert a transaction at the time of payment. Both Visa[4] and MasterCard[5] state that the rates they publish in advance of a transaction posting to a cardholder's statement are indicative, since the rates they use for conversion correspond to the date and time they process the transaction, as opposed to the actual transaction date.

With DCC, the currency conversion is done by the merchant or their bank at the point of sale. Unlike a credit card company, a DCC operator must disclose the exchange rate used for conversion at the time of the transaction according to credit card company rules which govern how DCC is offered.[2][3] The DCC exchange rate must be based on a wholesale interbank rate, to which any additional markup is then applied. Visa requires that this markup be disclosed to the cardholder.[2][3] The credit card company may still charge an additional fee for charges made outside the card holder's home country, even when the transaction has been processed in their home currency with DCC.

Proponents of this service believe that customers can better understand prices in their home currency, and this makes it easier for business travelers to keep track of their expenses. They also point out that the customer has full transparency inclusive of conversion fees, and can make an informed choice whether or not to use DCC. The financial benefit to the merchant or their card processor may be an incentive for the merchant to offer DCC even when it would be disadvantageous to the customer.

Opponents of the service believe that customers do not understand DCC, and point out that DCC exchange rate markups are mostly higher than the card issuers' currency conversion fees that DCC avoids, and therefore, in almost all cases, opting for DCC will result in a higher charge to the cardholder.

Due to the strategic threat posed by DCC on Visa's core revenues, in 2010 Visa attempted to ban DCC - The Australian federal courts found that Visa acted anti-competitively in order to protect its own revenues and was fined $20 million.

History

A dynamic currency conversion service was offered in 1996 and commercialized by a number of companies including Monex Financial Services[6] and FEXCO.[7]

Prior to the card schemes (Visa and MasterCard) imposing rules relating to DCC, cardholder transactions were converted without the need to disclose that the transaction was being converted into a customer's home currency, in a process known as "back office DCC". Visa and MasterCard now prohibit this practice and require the customer's consent for DCC, although many travelers have reported that this is not universally followed.[8][9]

Visa Chargeback reason code 76 explicitly covers situations where the "Cardholder was not advised that Dynamic Currency Conversion (DCC) would occur" or "Cardholder was refused the choice of paying in the merchant’s local currency". Customers have a strong chance of successfully disputing such transactions, especially in situations where they pay with a credit card and where Verified by Visa or Securecode is not involved. Mastercard DCC Compliance team investigates the case and then notifies the Acquirer of their findings. If appropriate, the Acquirer will also be asked to take action to remedy the complaint.

MasterCard take seriously any complaint from a customer by investigating the case for compliance with DCC rules, and if the customer was not given a choice in a DCC transaction, the customer's bank has the possibility to refund the customer with a chargeback sent to the merchant's bank.[10]

How it works

DCC is only available at merchants that have signed up for the facility with a DCC provider.

When a customer is ready to pay for a transaction and chooses to pay with a payment card, the point-of-sale terminal of a DCC merchant will determine the card's country of issue from the card's issuer identification number (first 6 digits of the card number). If it detects a foreign card is being used, then the transaction will be routed through the DCC provider, which may offer DCC to the customer.

If DCC is being offered, the terminal will also display the transaction amount in the customer's home currency. Visa and MasterCard require the DCC provider to disclose the exchange rate and margin to the cardholder, but not all merchants comply with this obligation, and other card issuers do not have that obligation. The cardholder can then select whether the transaction is to be processed in the local or home currency.

If the cardholder chooses to pay in their home currency, the DCC provider will cause the cardholder's account to be debited by the transaction amount in the home currency, and the merchant's account to be credited with the amount in the local currency. At regular periods, usually monthly, the merchant would also be credited with the commission for DCC transactions. The exchange rate risk is borne by the DCC provider, which may carry that risk or set up some hedging arrangement to minimise or transfer that risk.

Some card issuers impose an additional foreign transaction fee on DCC transactions, even though they are denominated in the card's home currency.

Practical example

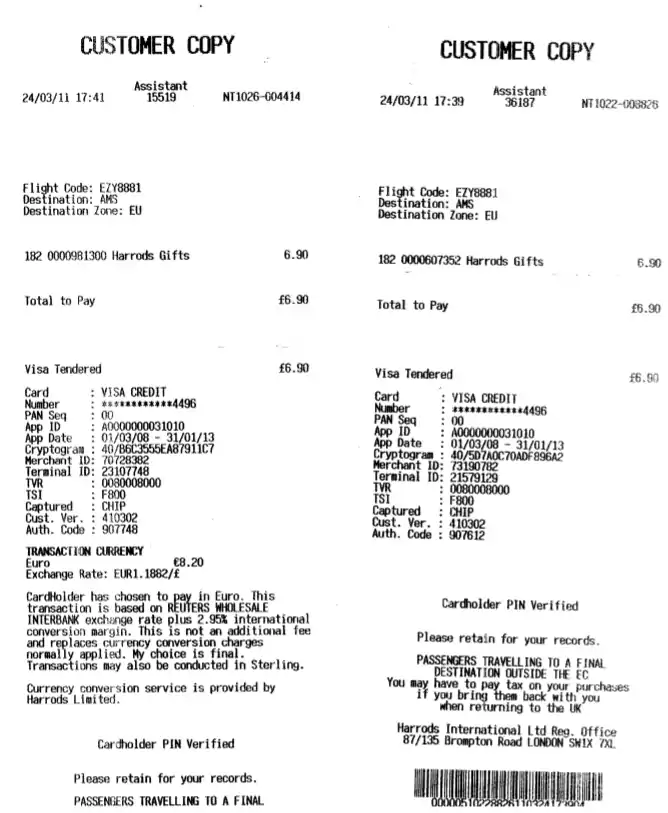

An example of the difference with DCC can be seen in the following image, where the same GBP purchase is made twice just after each other: one with DCC and one without DCC. In both cases, the original amount is GB£6.90 and is paid with a Visa card denominated in EUR.

The difference in charges can be seen on the customer's card statement. With DCC (left part of the above image), the amount becomes EUR 8.20, at an exchange rate of 1.1882. The DCC provider, in this example the merchant itself, also disclosed that it is using the Reuters Wholesale Interbank exchange rate plus 2.95%. Without DCC, the amount can vary with fluctuations between the GBP and EUR currencies, but on the date of this transaction it was EUR 8.04.

In this example, difference is just over 2%. Though this difference may seem a small amount for the customer, it can result in a big income stream for the DCC provider and merchant. One should also realise that even without DCC the card issuer converts the transaction amount using its own exchange rates and margins, which in this example was 1.16522.

Limitations

The merchant's point-of-sale terminal can only detect the card's country of issue and not the currency of the account that is to be selected. The DCC makes an assumption that the account home currency is the currency of the card's country of issue. This assumption can result in DCC being offered incorrectly. For example, a DCC-enabled terminal in the Eurozone will offer DCC to a customer paying with a debit card issued in the United Kingdom on a euro bank account. If the customer mistakenly chooses DCC, then the transaction will first be converted from EUR to GBP by the DCC provider, and then from GBP back to EUR by the UK card issuer, often with its markup.

There have reported cases of point-of-sale terminals allowing merchants to change the transaction amount and currency after the cardholder has entered their PIN and handed the terminal back to the merchant. In this scenario, DCC is carried out without the cardholder's consent, even though the receipt subsequently printed states falsely that the cardholder has given their consent.[11]

DCC on the Internet and ATMs

DCC operates similarly with Internet transactions. When payment card information is entered to finalize payment, the system can detect the home country of the cardholder and offer the cardholder the option of paying in their home currency.

Many commercial websites can detect the country from which a query has come and quote prices in terms of the enquirer's country. Often the prices in the local currency of the supplier are not indicated, and the exchange rate used to convert prices is often also not disclosed.

VISA issued a rule making DCC available for cash withdrawals at ATMs as of 13 April 2019. Mastercard now does the same.

In the VISA example, when DCC is NOT chosen, VISA converts currency at the wholesale (!) rate and adds a 1% charge for performing the conversion. The customer gets the "real" exchange rate (no commission) unless the card issuer adds a charge for international transactions. American banks, for example, often charge 3%, even though the debit order they receive is already presented for collection in US dollars. Some banks and other issuers make no extra charge, so the full international transaction cost is just the 1%.

When DCC is applied, the alternate companies do the exchange and add the commissions described above, which have no limit. The bank card company, such as VISA, still takes its 1%.

VISA rule 5.9.8.3 of 13 April 2019 says that ATM customers must be given a clear CHOICE whether to use DCC or not:

"A Merchant or ATM Acquirer that offers Dynamic Currency Conversion (DCC) must comply with all of the following: . . . "5 Acceptance

"-- Inform the Cardholder that DCC is optional and not use any language or procedures that may cause the Cardholder to choose DCC by default

"-- Ensure that the Cardholder is given all the relevant information to allow them to make a clear and transparent decision to expressly agree to a DCC Transaction"

The reality is otherwise. The screen on an ATM announces the exchange rate that will be used and asks whether the customer accepts or refuses that rate. It appears to be "take it or leave it." There is NO explanation that refusal will not end the transaction, but rather means the exchange will be done without charging the commission. The clear "choice" required by the rule is not presented. In addition, there is usually very small type giving the % of the commission and saying this is not an additional charge (which is false). On some screens there will be advice to be sure to know the rules, but no way is provided to learn the rules and bank tellers are generally unaware of them.

Impact

DCC has proved popular with merchants because it enables them to profit from the foreign exchange conversion that occurs during the payment process for a foreign denominated credit card.[12]

Credit card acquirers and payment gateways will also take a profit on the foreign exchange conversion that occurs during the payment process for foreign denominated credit card when DCC is used. DCC revenue has been important for them because it offsets increasing international interchange fees.

Advantages

The main advantage of DCC is that for a non-DCC transaction the customer does not know exactly the exchange rate that the credit card company will apply (and the final cost) until the transaction is cleared, so the actual rate is not known to the customer until it appears on a monthly statement.

Other advantages to customers, according to proponents, are:

- the ability to view and therefore understand prices in foreign countries in their home currency,

- the ability to enter expenses more efficiently and promptly, especially for business travellers, and

- EU regulation 2560/2001 could make non-eurozone cash withdrawals within the European Economic Area cheaper for eurozone customers because euro cash withdrawals are regulated. A Swedish law (SFS 2002:598) combined with the EU resolution does the same thing for Swedish cards if the transaction is in SEK or EUR. Generally, Eurozone banks charge a fixed fee for non-EEA and non-EUR cash withdrawals while EEA withdrawals in EUR are free of charge. For example, if a Eurozone card is used for a withdrawal in the UK, with DCC there are two options - processing the transaction in GBP (card issuer's exchange rate but a fixed cash withdrawal fee) or processing the transaction in EUR (DCC marked-up exchange rate but no fixed cash withdrawal fee). For small amounts, the latter option will often be cheaper.

For the merchant which normally accepts credit cards, DCC offers an opportunity to earn a margin on the transaction with no exchange rate risk, which is borne by the DCC operator.

Disadvantages

The main objection to DCC is the unfavorable exchange rates and fees being applied on the transaction,[13] resulting in a higher charge on their credit card, and that in many cases the customer is not aware of the additional and often unnecessary cost of the DCC transaction.

The size of the foreign exchange margin added using DCC varies depending on the DCC operator, card acquirer or payment gateway and merchant. This margin is in addition to any charges levied by the customer's bank or credit card company for a foreign purchase. In most cases, customers are charged more using DCC than they would have been if they had simply paid in the foreign currency.[13][14]

Regulatory issues

In May 2010 Visa Inc attempted to ban DCC on its network citing strategic issues and ultimately (as described by the ACCC) significant financial losses to its business. Many protests were made by merchants, financial institutions, and regulators.

In 2015, Visa was fined approximately A$18 million plus $2 million in costs for engaging in anti-competitive conduct, in proceedings brought by the Australian Competition and Consumer Commission. The action was taken after Visa partially blocked the use of DCC 1 May 2010 to 6 October 2010.[15]

DCC providers

The main DCC providers are:

- Alliex Co.,Ltd[16] based in South Korea

- ConCardis[17] based in Germany

- Cuscal Ltd[18] based in Australia

- Euronet Worldwide[19] based in the United States

- Pure Commerce based in Australia

- Continuum Commerce Solutions[20] based in Ireland

- Elavon[21] based in USA

- FEXCO Dynamic Currency Conversion[22] based in Ireland

- First Data[23] based in the United States

- Global Blue[24] based in Switzerland

- Monex Financial Services[25] based in Ireland

- Planet Payment[26] based in the United States

- Premier Tax Free, part of the Fintrax Group[27] based in Ireland

- Six Payment Services[28] based in Switzerland

- Travelex[29] based in the United Kingdom

- Worldline[30] based in the United States

References

- Guy, Anker (4 July 2016). "The worst 'paying in pounds abroad' rip-off I've seen – where £160 of cash costs £190". MoneySavingExpert. Retrieved 30 August 2017.

- https://usa.visa.com/dam/VCOM/download/merchants/visa-international-operating-regulations-main.pdf

- http://www.mastercard.com/elearning/dcc/docs/DCC%20Guide%2020.02.17%20EN.pdf

- "ExchangeRateComp - Visa". usa.visa.com.

- "Currency Converter - Foreign Exchange Rates Calculator - Mastercard". www.mastercard.us.

- Monex Financial Services - Dynamic currency conversion

- "Dynamic Currency Conversion (DCC)". FEXCO. Retrieved 9 June 2014.

- Collinson, Patrick (12 July 2008). "Going to Spain? Just say no". The Guardian. London. Retrieved 1 May 2010.

- "Dynamic currency exchange". FlyerTalk. Retrieved 31 December 2011.

- "Dynamic Currency Conversion Compliance Guide, MasterCard, 2016" (PDF).

- Megan, French (17 August 2017). "Avoid holiday rip-offs by ALWAYS keeping hold of the card machine AFTER entering your PIN". MoneySavingExpert. Retrieved 30 August 2017.

- Yang, Maximilian, 'Dynamic Currency Conversion – ein grenzüberschreitendes verbraucherpolitisches Problem' (Dynamic Currency Conversion – a cross-border consumer policy problem), [2015] BKR 407, 408 (in German), with further references.

- Keck, Gayle (31 July 2005). "Charge It . . . but Check the Math". Washington Post. Retrieved 31 December 2011.

- "Dynamic Currency Conversion: Still A Scam". 9 March 2008. courant.com. Archived from the original on 9 November 2012. Retrieved 31 December 2011.

- "Visa ordered to pay $18 million penalty for anti-competitive conduct following ACCC action". Australian Competition and Consumer Commission. 4 September 2015. Retrieved 16 December 2018.

- "Alliex - DCC, MCP". www.alli-ex.com.

- "Concardis Optipay". www.concardis-optipay.com.

- "Cuscal Limited". www.cuscalpayments.com.au.

- "Pure Commerce: Dynamic Currency Conversion, Multi Currency Pricing, Multi Currency Processing". www.pure-commerce.com.

- "home". www.Continuumcommerce.com.

- "Dynamic Currency Conversion (DCC)". www.elavon.co.uk.

- "Introduction - Dynamic Currency Conversion - FEXCO".

- "Dynamic Currency Conversion (DCC)". First Data.

- "Shopping guide, Guide to shopping abroad - Global Blue official site". globalblue.

- "Dynamic Currency Conversion DCC - Monex". monexfinancialservices.

- "Planet Payment - Delivers innovative payment processing solutions". Planet Payment.

- "Home". Fintrax.

- "Payment Services – SIX". SIX.

- "Currency Exchange & Travel Money at Great Rates - Travelex". www.travelex.com.au.

- "Global leader in e-payment transactional services". worldline.com.